Buying a home in Canada can feel like trying to solve a Rubik’s cube blindfolded, especially if you’re new to the country. But don’t worry, there are programs out there to help immigrants snag their first home sweet home.

Let’s check out some mortgage programs and insurance options that are perfect for newcomers.

Special Mortgage Programs

Canadian banks have rolled out the welcome mat with mortgage programs just for immigrants. These are great for folks with a short credit history or those with a work permit in hand.

CIBC Newcomer to Canada Program Mortgage

The CIBC Newcomer to Canada Program Mortgage is like a friendly neighbor offering a hand. New immigrants can get a home with just a 5% down payment if the house costs $1 million or less. If you’re eyeing something pricier, you’ll need to cough up 35% or more.

CIBC Newcomer to Canada PLUS Program Mortgage

The PLUS version of the CIBC Newcomer to Canada Program Mortgage throws in some extra goodies like flexible down payments and sweet interest rates. It’s a good fit for those who’ve been in Canada for at least three months and can show they can handle the monthly payments.

CIBC Foreign Worker Program Mortgage

Got a work permit? The CIBC Foreign Worker Program Mortgage is your ticket. With a down payment as low as 5%, foreign workers who’ve been in Canada for three months and can prove they’re employed can get in on the action.

Mortgage Insurance Options

Mortgage insurance is like a safety net for newcomers. It helps reduce the risk for banks if you can’t make payments and lets you get a mortgage with a smaller down payment.

Mortgage Loan Insurance Programs

These programs are a lifesaver for newcomers. With just a 5% down payment, they offer financial protection to lenders. The Home Buyers’ Plan (HBP) and the First-Time Home Buyers’ Savings Account (FHSA) are popular choices for first-time buyers.

Newcomers to Canada Program

The “Newcomers to Canada program” are various initiatives designed to support individuals who have recently moved to Canada. One of the initiatives is the CIBC Newcomer to Canada Program Mortgage. It is specifically designed for newcomers to Canada, allowing them to qualify for a mortgage even with limited or no Canadian credit history [as previously discussed above].

You can buy a home with just a 5% down payment if it’s $1 million or less. For anything over that, you’ll need to put down 35% or more. There’s no cap on the mortgage amount, but the home price must be $1 million or lower.

To learn the saving strategies for a down payment in Canada, read this article about the ‘Best Saving Strategies for a Down Payment’

Financial Requirements for Buying a Home in Calgary, Alberta

Buying a home in Canada, especially for immigrants or folks moving from pricier provinces to Calgary, Alberta, can feel very overwhelming. Here’s a breakdown of the basics of what you need to know about down payments and credit scores.

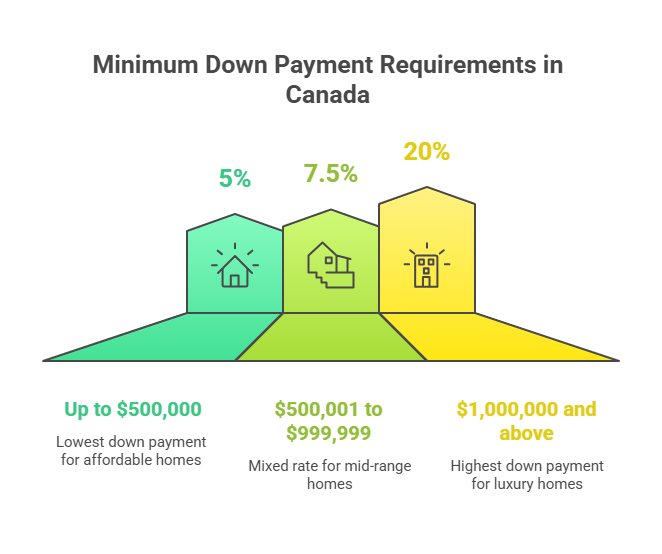

Down Payment Guidelines

In Canada, the down payment is a important when you’re buying a house. How much you need depends on the price tag of the home. If you’re new to this, study the chart below to know the minimum down payment rules so that you may understand how mortgage insurance works.

If your down payment is less than 20%, you’ll need mortgage loan insurance. This insurance helps protect the bank if you can’t make your payments. Some places have special insurance programs for newcomers with just a 5% down payment.

There’s also the Home Buyers’ Plan (HBP), which lets you pull out up to $35,000 from your RRSP (Registered Retirement Savings Plan) without paying taxes to buy or build your first home. However, you must make sure the money has been in the RRSP for at least 90 days before you take it out. After you get the money, you’ve got 15 years to pay it back.

Credit Score History Considerations for New Comers

Newcomers to Canada typically start with no credit score, as their credit history from their country of origin does not transfer to Canada.

This means they begin building their Canadian credit history from scratch. While a good credit score is essential for securing loans and mortgages, some programs are designed to accommodate newcomers with limited or no Canadian credit history.

For instance, the CMHC Newcomers Program requires a minimum credit score of 600 for at least one borrower or guarantor, and may consider alternative methods of establishing creditworthiness if a Canadian credit history is limited.

Additionally, banks like Scotiabank offer credit cards under the StartRight® Program without requiring a Canadian credit history. As newcomers build their credit, they can improve their scores by using credit responsibly and making timely payments.

Learn how buying a home affects your credit score in Canada here.

Government Programs for First Time Homebuyers

In Canada, there are government programs ready to lend a hand to first-time homebuyers.

Here are the two big ones: the First-Time Home Buyer Incentive and the Shared Equity Mortgage Providers Fund.

First-Time Home Buyer Incentive (FTHBI)

The First-Time Home Buyer Incentive is part of Canada’s National Housing Strategy, designed to help first time home buyers acquire their first home (Government of Canada).

This program aims to make homeownership more affordable by providing a government loan of either 5% or 10% of the purchase price, which goes towards the down payment.

Key Features:

- The government chips in 5% or 10% of the home’s price for your down payment.

- This amount helps shrink your monthly mortgage bill.

- You must pay it back after 25 years or when you sell the home.

The program has been extended until March 31, 2025, to continue supporting first-time buyers. To check eligibility, click here

Shared Equity Mortgage Providers Fund

This fund supports shared equity mortgage providers, helping eligible Canadians achieve affordable home ownership. It encourages additional housing supply and attracts new providers of shared equity mortgages.

Key Features:

- Offers cash to shared equity mortgage providers.

- Pushes for creative homeownership ideas.

- Helps build more affordable housing.

Learn more about this fund by clicking here.

By tapping into these government programs, immigrants and those moving to wallet-friendlier cities like Calgary, Alberta, can get the boost they need to make their homeownership dreams come true.

For more tips and resources, dive into our article on the Canada home buying process made simple for newcomers, in this link.

Where to Get Assistance You Can Trust as a New Comer

For a successful home buying process, you need to work with a knowledgeable Realtor. They can guide you through the process of helping you navigate Calgary’s neighborhoods, know best financing options and ensure you understand the local market conditions. Get you perfect realtor match using our tips in this article.

For newcomers to Calgary seeking reliable information on buying a home, reading from trustworthy sources such as this Jenga Homes blog. In our easy to read and informative articles, newcomers can gain a deeper understanding of Calgary’s real estate landscape, learn how to save, Canadian credit scores, getting pre-approved for a mortgage, how your employment affects the home buying process, home inspections, common homeownership hidden costs and so much more!

For situation specific questions, don’t hesitate to contact us on (403)-472-3909.

Before you go, grab your Free copy of our Calgary Home Buying Glossary for new comers. This downloadable will help you understand the home buying language and save you from misunderstandings that can cost you money and time. It’s Free! Get it here now!