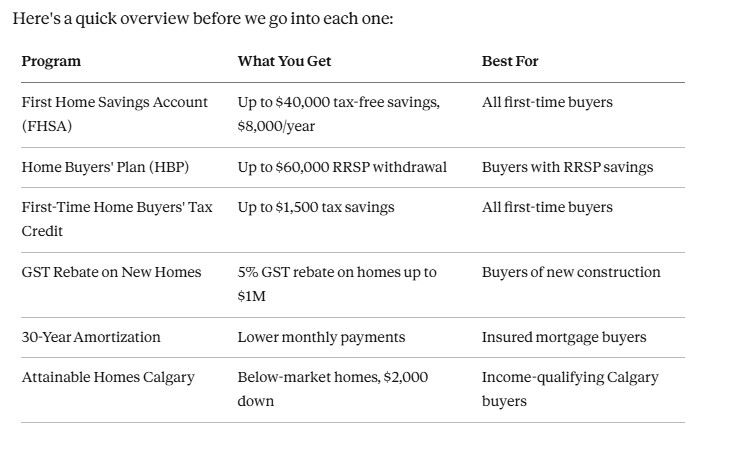

First-time home buyers in Alberta can access several federal programs in 2026: the First Home Savings Account (FHSA, up to $40,000 lifetime), the Home Buyers’ Plan ($60,000 RRSP withdrawal), the First-Time Home Buyers’ Tax Credit ($1,500 back), a 5% GST rebate on new homes, and 30-year amortization.

Calgary buyers can also access Attainable Homes Calgary. Used together, these programs can save you tens of thousands of dollars.

Buying your first home in Alberta is a big deal. Good news is that it’s also more achievable than many buyers realise, because there are real programs designed to help you get there. The challenge is knowing which ones still exist, which have ended, and how to combine the ones that work.

If you’ve been searching for first-time home buyer incentives in Alberta, you’ve probably come across some confusing or outdated information. Some articles still mention the federal First-Time Home Buyer Incentive (FTHBI), which was cancelled in March 2024. Others mix up programs that apply in Alberta with ones that don’t.

This guide covers the programs that are actually available to Alberta buyers in 2026, what each one offers, who qualifies, and how to use them together when buying a new home. At Jenga Homes, we help first-time buyers in Calgary and High River navigate this process every day. Here’s what you need to know.

What First-Time Home Buyer Incentives Are Available in Alberta in 2026?

First-time buyers in Alberta can access five core programs in 2026: the First Home Savings Account (FHSA), the Home Buyers’ Plan (HBP), the First-Time Home Buyers’ Tax Credit, a 5% GST rebate on new homes under $1 million, and the 30-year amortization option. Calgary buyers may also qualify for Attainable Homes Calgary. The federal First-Time Home Buyer Incentive (FTHBI) is no longer available — it was discontinued in March 2024.

What Is the First Home Savings Account (FHSA) and How Does It Work?

The FHSA is the most powerful savings tool available to Canadian first-time buyers in 2026. You can contribute up to $8,000 per year to a lifetime maximum of $40,000. Contributions are tax-deductible like an RRSP, and qualifying withdrawals for a home purchase are completely tax-free like a TFSA. No other registered account in Canada gives you both benefits at once.

Introduced in 2023, the FHSA has become the default first step for any first-time buyer with time to save. Here’s how it works in practice:

Contribution limits: The 2026 annual FHSA contribution limit is $8,000, with a lifetime cap of $40,000. If you didn’t contribute the full $8,000 in a previous year, you can carry forward up to $8,000 of unused room to the following year. So if you opened an FHSA in 2025 and only contributed $3,000, you can contribute up to $13,000 in 2026.

The tax benefit: Every dollar you contribute reduces your taxable income, just like an RRSP contribution. If you earn $70,000 and contribute $8,000, you’re taxed as if you earned $62,000. Depending on your tax bracket, that’s a refund of $1,700 to $3,800.

The withdrawal: When you use your FHSA to buy a qualifying home, the entire amount (contributions plus any investment growth) comes out completely tax-free. There’s no repayment required, unlike the Home Buyers’ Plan.

Couples: Each partner can open their own FHSA. A couple who both max out their accounts can accumulate up to $80,000 in tax-free down payment savings together.

Important deadline note: FHSA contributions must be made by December 31. Unlike RRSPs, there’s no 60-day grace period into the new year.

If you’re buying a new home and have even a few years to save, opening an FHSA today is one of the smartest financial moves you can make. Even contributing $1 starts your room accumulating.

How Does the Home Buyers' Plan (HBP) Work for Alberta Buyers?

The Home Buyers’ Plan lets you withdraw up to $60,000 from your RRSP tax-free to use as a down payment on your first home. Couples can combine for up to $120,000. You have 15 years to repay the amount, starting two years after the withdrawal. Unlike the FHSA, the HBP requires repayment, but it’s still a significant source of down payment funds for buyers who have been saving in an RRSP.

The HBP is administered by the Canada Revenue Agency and applies across Canada, including Alberta.

A few things to know before you use it:

- Your RRSP funds must have been in the account for at least 90 days before you withdraw them under the HBP.

- If you don’t repay the required annual amount, it gets added to your taxable income for that year.

- You can use both the HBP and the FHSA for the same home purchase. A couple combining both programs could access up to $200,000 in tax-advantaged down payment funds.

The smart strategy is to prioritise the FHSA first (no repayment required) and then supplement with the HBP if you need additional funds.

What Is the First-Time Home Buyers' Tax Credit?

The First-Time Home Buyers’ Tax Credit gives you a non-refundable federal tax credit worth up to $1,500 in the year you buy your first home. It applies to all qualifying first-time buyers in Canada, including Alberta. You claim it on your income tax return for the year you purchased.

To claim it, you purchase a qualifying home and file your taxes as a first-time buyer. The credit is based on $10,000 at a 15% tax rate, which works out to $1,500. Couples can split the credit between them, but the total can’t exceed $1,500 combined.

It’s not a fortune, but it’s money you’re entitled to that costs nothing extra and requires no advance action. Just make sure you or your accountant claims it the year you buy.

What Is the GST Rebate on New Homes?

New homes priced under $1 million in Canada are subject to 5% GST. Since 2025, qualifying buyers receive a full 5% GST rebate on new home purchases up to $1 million, phasing out at $1.5 million. For a new home priced at $450,000, that’s a $22,500 saving. The rebate is typically applied directly by the builder, reducing the purchase price you pay.

This is one of the most underappreciated incentives for buyers of new construction. If you’re buying a newly built home in Calgary or High River, the GST rebate represents real, immediate savings.

At Jenga Homes, we build homes from $400,000. The GST rebate on new housing applies to all our current projects and is factored into your purchase pricing. Your dedicated Jenga contact can walk you through exactly how this applies to the home you’re considering.

What Is the 30-Year Amortization Option?

As of late 2024, first-time buyers purchasing a new home in Canada can amortize their insured mortgage over 30 years instead of the previous maximum of 25 years. This lowers your monthly mortgage payment and makes qualifying easier on a tighter income. It applies to insured mortgages (those with a down payment under 20%) on new construction homes.

The practical effect is meaningful. On a $450,000 mortgage at a typical rate, extending from 25 to 30 years reduces the monthly payment by roughly $200 to $300. That can be the difference between qualifying and not qualifying for many first-time buyers.

The trade-off is that you pay more interest over the life of the mortgage. But for buyers who need the breathing room now, it’s a genuine affordability tool.

What About Attainable Homes Calgary?

Attainable Homes Calgary (AHC) is a non-profit, City of Calgary-owned program that helps workforce buyers purchase quality homes below market price, with as little as $2,000 as a down payment. To qualify in 2026, household income must be under approximately $131,424, assets must be below $50,000, and buyers must obtain mortgage pre-approval through AHC’s partner lenders.

The Attainable Homes Calgary program uses a shared appreciation model. The buyer’s equity percentage increases over time. Buyers must complete a home education session as part of the process.

AHC isn’t for everyone. The income cap and asset limit mean it targets buyers who are genuinely moderate-income. But for buyers who qualify, it’s one of the most significant affordability tools available in Calgary.

Note: If you’re considering an AHC home alongside a Jenga Homes build, our team can help you think through both paths and what makes sense for your situation. Reach out for a no-pressure conversation.

What Happened to the First-Time Home Buyer Incentive (FTHBI)?

The federal First-Time Home Buyer Incentive (FTHBI) was permanently discontinued in March 2024. No new applications have been accepted since March 21, 2024, and no new approvals were granted after March 31, 2024. If you’ve read about this program elsewhere, that information is outdated. It no longer exists.

The CMHC cancelled the FTHBI because the program was significantly undersubscribed. Of the 100,000 buyers it was designed to help, fewer than 16,000 applications were ever received. The income limits and property price caps were too restrictive for most Canadian markets, including Calgary.

If you participated in the FTHBI before it ended, your obligations remain unchanged. You still owe repayment within 25 years or upon sale of your home.

For everyone else: the FHSA, HBP, tax credit, GST rebate, and 30-year amortization are the programs that replace it. They’re collectively more useful for most buyers anyway.

How Can I Combine These Programs to Maximise My Buying Power?

Most first-time buyers in Alberta can use multiple programs simultaneously. The most powerful combination is the FHSA plus the Home Buyers’ Plan: together, a couple can access up to $200,000 in tax-advantaged down payment funds. Add the GST rebate on new construction, the 30-year amortization option, and the First-Time Home Buyers’ Tax Credit, and the total benefit can easily exceed $30,000 in real savings.

Here’s what a realistic combination looks like for a single buyer purchasing a new Jenga Homes build at $450,000:

- FHSA: $40,000 saved, fully tax-free at withdrawal. Tax deductions during saving years saved roughly $8,000 in tax.

- HBP: $30,000 RRSP withdrawal to supplement the down payment.

- GST rebate: $22,500 saving on the purchase price.

- First-Time Home Buyers’ Tax Credit: $1,500 back at tax time.

- 30-year amortization: Lower monthly payments, improving mortgage qualification.

Total in real savings and tax benefits: well over $30,000, depending on income and savings history.

The key is starting early. Opening an FHSA and contributing even a modest amount each year builds both the account balance and the contribution room you can use later.

Can I Use These Incentives to Buy a New Build Home?

Yes. All of the programs listed above apply to new construction homes, and in the case of the GST rebate and 30-year amortization, new construction is specifically advantaged. Buying a new home from a fixed-price builder like Jenga Homes means you know the exact purchase price before you sign, which makes planning your incentive strategy straightforward.

At Jenga Homes, we work with first-time buyers in Calgary and High River who are using these programs. Our fixed-price contracts mean your budget is protected from day one: no material cost overruns, no surprise invoices. You know what you’re paying before you commit.

We also connect buyers with trusted mortgage partners who understand how to structure these programs together for maximum benefit.

If you’re ready to understand what your budget can actually buy in 2026, browse our current and upcoming homes or book a free call with our team. No pressure, no jargon. Just an honest conversation about what’s possible.

In Conclusion...

There has never been a broader toolkit available to first-time buyers in Alberta than what exists in 2026. The FHSA, HBP, tax credit, GST rebate, and 30-year amortization work together to reduce your upfront costs, lower your monthly payments, and put real money back in your pocket.

The federal FTHBI is gone. But the programs that replaced it are more flexible and more useful for most buyers.

The biggest mistake first-time buyers make is waiting to learn about these programs until they’re ready to buy. The FHSA in particular rewards buyers who open it early, even years before they’re ready to purchase. Every year you wait is a year of contribution room and tax-free growth you don’t get back.

At Jenga Homes, we build quality new homes in established Calgary communities and High River, starting from $400,000. Read the blogs we write that explain the full purchase process in plain English.

And our team is always available to walk you through how these programs apply to the home you’re considering.

Contact Jenga Homes today and let’s talk about your first step into homeownership.

Frequently Asked Questions

Q: What first-time home buyer programs are available in Alberta in 2026?

A: The main programs available to Alberta first-time buyers in 2026 are: the First Home Savings Account (FHSA, up to $40,000 lifetime), the Home Buyers’ Plan ($60,000 RRSP withdrawal per person), the First-Time Home Buyers’ Tax Credit ($1,500 back), a 5% GST rebate on new homes under $1 million, and the 30-year amortization option for new home buyers. Calgary buyers may also qualify for Attainable Homes Calgary.

Q: Is the First-Time Home Buyer Incentive (FTHBI) still available in 2026?

A: No. The federal First-Time Home Buyer Incentive (FTHBI) was permanently discontinued in March 2024. No new applications have been accepted since March 21, 2024, and no new approvals were granted after March 31, 2024. If you participated in the program before it ended, your repayment obligations remain unchanged.

Q: How much can I withdraw from my RRSP under the Home Buyers’ Plan in 2026?

A: You can withdraw up to $60,000 per person from your RRSP tax-free under the Home Buyers’ Plan. A couple can combine their withdrawals for up to $120,000. The funds must have been in your RRSP for at least 90 days before withdrawal, and you have 15 years to repay the amount starting two years after you withdrew it.

Q: What is the FHSA annual contribution limit in 2026?

A: The FHSA annual contribution limit in 2026 is $8,000, with a lifetime maximum of $40,000. If you didn’t contribute the full $8,000 in a previous year, you can carry forward up to $8,000 of unused contribution room. For example, if you opened an FHSA in 2025 and contributed $3,000, you can contribute up to $13,000 in 2026. The contribution deadline is December 31 each year.

Q: Can I use both the FHSA and the Home Buyers’ Plan for the same home purchase?

A: Yes. You can use both the FHSA and the Home Buyers’ Plan (HBP) toward the same home purchase. For a couple, this means up to $80,000 from two FHSAs and up to $120,000 from two RRSPs under the HBP, for a combined total of up to $200,000 in tax-advantaged down payment funds. The FHSA has no repayment requirement; the HBP must be repaid over 15 years.